US$ Euro Yen

North America

Caribbean

Central America

South America

Western Europe

Eastern Europe

Russia

Former USSR

Middle East

North Africa

West Africa

East Africa

Southern Africa

South Asia

Pacific Rim

Commodities

Multinational

April 2, 2026 (see April 14 and April 22 updates below). Next update: May 4, 2026. Visit Search to look at past issues of World Currency Observer (brochure edition).

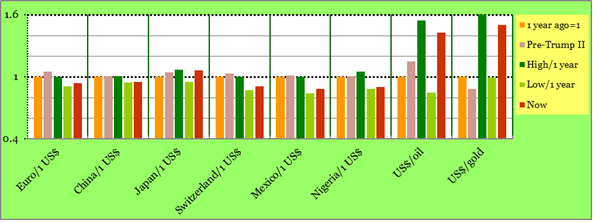

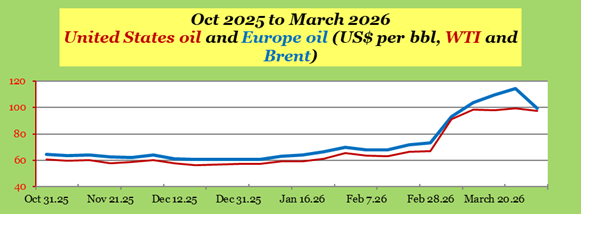

Exchange rate developments in March 2026 were largely dominated by the disruption of worldwide petroleum and shipping markets, attributed to closure of the Strait of Hormuz route for the export of oil and other shipments, after the February 28 start of the United States attack on Iran (and also the destruction of infrastructure in neighboring countries around the Persian Gulf and the Gulf of Oman), contributing to significant worldwide increases in petroleum prices in March (the oil price rises include both the Europe-centered Brent oil price, and a lesser rise in the United States-centered West Texas Intermediate oil price). The impact on foreign exchange markets around the world in March 2026 has been a decrease in the US$ value of nearly every currency around the world, i.e., a general rise in the value of the US dollar. The few exceptions to currency weakness against the US$ in March 2026 included: the Argentina peso (which has been going through extensive economic and financial reforms, which include stabilizing the value of the Argentina peso); the Kazakhstan tenge (which is, at a moment when world oil prices have shot up, an oil exporter with large oil and natural gas reserves, bordering China and Russia, and which is in a strategic geographic location with access to most Asia and Europe markets at a time of oil and gas disruptions); and also included the Colombia peso, the Costa Rica colón and the Madagascar ariary - more on these currencies later. The strength of the US dollar in March is attributed to what is generally referred to as the (complex) safe haven status of the United States dollar. It should be added that another of the world's safe haven currencies, the Swiss franc, fell by 4% in March against the US dollar, with the fall beginning immediately after the start of the United States attack. There was a similar fall in the Japanese yen (where thought is being given to raising interest rates throughout the rest of 2026). The Euro was down by 2.5% in March, and the China yuan was down by 0.75%. Also, a symptom of the flight to the US dollar in March has been the drop over the month in US$ market prices for gold (down by 12%) and silver (down by 19%).

The United States blockade of shipments encompassing Iran ports in and near the Strait of Hormuz, with a particular effect on oil and gas, went into effect earlier this week (there are also Iranian mines in the Strait which the United States is working to clear). There are many implications of the restrictions in supply beside higher world oil prices - as widely noted, among the expected impacts are a reduction in world fertilizer supply, particularly in Africa, with higher world food prices expected. Also, the US might not be paying enough attention to its fiscal position, particularly as it relates to tariff issues. Among the exchange rate-related events so far this month: there was a three-week period in late March-early April when the US$ price of US-based WTI oil exceeded the European Brent oil price, which was reversed this week. Currencies around the world have generally been getting stronger against the US$ in April 2026, with a temporary reversal around the first week of April, when the United States suggested it was going to bomb bridges and power plants in Iran, a threat which was quickly rescinded.

Syria (adjacent to Türkiye, Iraq, Lebanon, Jordan and Israel, with several ports on the Mediterranean, and accessible by land, across Iraq, to the Strait of Hormuz)) is in the midst of what was originally visualized as a year-long transition to new currency notes, with a redenomination of 100 of the old lira (pound) notes to one new lira (pound), from currency notes with Assad family images, to new currency notes with images of Syria natural resources (Syria new currency notes are clearly intended to signal a break with its recent authoritarian and civil war past, with emphasis on agricultural production– the new notes include 500 lira with a wheat image, 200 with olive trees, 100 with cotton plants, 50 with oranges, 25 with grapes and 10 with rose plants). The transition started on January 1 2026, with a target completion date initially set, in the middle of last year, at December 8, 2026, a deadline which was later revised to having the transition completed in the first 90 days (this transition has just been revised again, to the end of May 2026). Until the transition is completed, there are currently two Syria lira quotations, with quotations in the media placing more emphasis on the old lira, i.e., the lira rate for 1$US quoted this week in the media is 12800, while the rate indicated on the central bank web site is in new lira 110/111per 1$US. There are some variations in lira/US dollar and lira/ Türkiye lira exchange rates among the cities of Syria (Damascus, Aleppo etc), especially between border cities (more emphasis on foreign trade) and those in the interior of the country, and on the varying local degrees of reliance on the old lira or the new lira. The new lira is to be used for bank operations, exchange companies and offices, and for contracts, and the new lira is the exchange rate for foreign remittances. The lira has been positively impacted so far in 2026, including the transfer of oil and gas fields from army to national control. Like other currencies around the world, the Syria lira fell sharply following the Feb 28 date of the American invasion of Iran, and has strengthened in the past few days. There was a great deal of emotional reaction within the country to the new currency, focusing on the design of the new currency and what it meant for the future of Syria, breaking with the past, after many years of the Assad family and fourteen years of civil war. Also proceeding is movement to restore cross-border currency links, such as connections through SWIFT (initiated in February 2026 and still being fully implemented) and correspondent banking relations. In the last few days, the Syria lira old lira has strengthened from the 13350 per 1$US low it reached on April 14, and is now at under 13000 – the old lira was below 12000 in the middle of March 2026.

(World Currency Observer will next be updated on May 4, 2026. Visit Search to look at past issues of World Currency Observer (brochure edition). For permission-to-quote enquiries, e-mail World Currency Observer at WCO@briargreen.com.)