US$ Euro Yen

North America

Caribbean

Central America

South America

Western Europe

Eastern Europe

Russia

Former USSR

Middle East

North Africa

West Africa

East Africa

Southern Africa

South Asia

Pacific Rim

Commodities

Multinational

January 2, 2026 (see January 20 update below). Next update: February 2, 2026. Visit Search to look at past issues of World Currency Observer (brochure edition).

A vast majority of currencies of the countries around the world moved up against the US$ in 2025, with the weakness in the US$ most pronounced in the first six months of the year - the US$ generally continued to move down after that, but at a more gradual pace. The decline in the US$ was steeper against the more advanced economies of the world than against the less advanced. Notable exceptions to the upward movement against the US$ included the Japan yen (with essentially no net change in 2025 - strengthening through the first four months of the year, which was then balanced by continual weakening of the yen until the end of 2025), the India rupee (some of its neighboring country currencies also showed net weakness against the US$), and the high inflation countries, which include Argentina, Iran, Turkey and Venezuela. Major economic events around the world which would normally affect currencies included the comprehensive increases in tariffs on goods traded into the United States (offset with limited retaliation in this very one-sided trade war, with the major exception being China versus the U.S.), and it is interesting that the 2025 increases in US tariffs (other influences ignored, predicted to improve the trade balance and strengthen the exchange rate) have been accompanied, so far, by a general weakening of the US$.

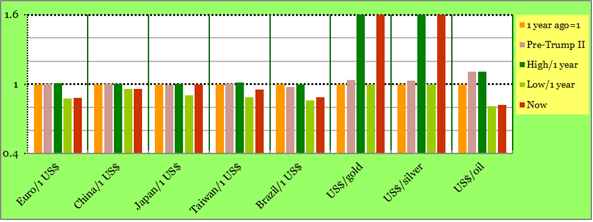

North America currencies - Canada dollar, Iceland króna and Mexico peso - were up against the US$ over the month of December 2025 and over the entire year of 2025. The Dominican Republic peso was down by 3.75% against the US$ since this time last year, and the Jamaica dollar was down by 3%. South America currencies were mostly stronger against the US$ over 2025. Exceptions included the Argentina peso and Venezuela bolivar, but also the Suriname guilder, which was down by 8.25% on the year (but was up by 1.5% against the US$ in December 2025, after rising in October and November) - Suriname is expecting a windfall to come from upcoming oil and gas production, but is currently in what has been characterized as a pre-production phase, with a current account deficit generally attributed to high imports of goods and services needed to move to the high production expected to come. As remarked above, the Euro was up by nearly 12% on the year (the United Kingdom pound was up by 7% over the same period), and, in December 2025 alone, the Euro was up by nearly 1.25% against the US$. The Türkiye lira was down 22% on the year against the US$, with a 1% downward movement in December 2025. Currencies of countries of the former USSR were generally up against the US$, both in December 2025 only and in 2025 in general, with the exception being Ukraine, which showed almost no net exchange rate movement. Currencies in the Middle East were generally up against the US$ in December 2025 and over the entire 2025 - a notable exception has been Iran, with a widely publicized 20+% collapse in the US$ value of the rial in December 2025, which is now down by 65% over the whole of 2025. The Israel shekel was up by 14% in 2025 against the US$. Africa currencies were almost unanimously up against the US$ over the month of December 2025 and over 2025 in general - among the exceptions were Rwanda (down 5.5% on the year), Tanzania (down 2.5% on the year against the US$) and Burundi (down 2% over 2025). The Indonesia rupiah was down by 3.4% against the US$ over the last year, and the Philippines peso was down by 1.75%. The India rupiah was down by 5% against the US$ over the last year, and the currencies of some surrounding countries were also down, including the Sri Lanka rupee (down 6%), and the Bangladesh taka (down 2.5% against the US$). The Myanmar kyat was up by 3.25% against the US$ in December 2025, and up by nearly 9% over the last year. The Vietnam dong was down by 3.25% against the US$ over the last year. Gold prices in US dollars are up by 67% since this time a year ago, and petroleum prices are down by 18% over the same period. Copper prices were up by 12% in December 2025, and up by 39% since this time last year. Cocoa and coffee prices are down from their level at this time last year, but are still very high in historical terms.

Bulgaria (population of around 6.7 million) totally ended the use of its 145 year old currency, the leva, over the 3 days of Dec 31/25-January 2/26, at the 1.95583 Euros per lev exchange rate to which it has been locked-in since the Euro was introduced in 1999 (as such, the leva remained within its longstanding +/-2.25% band, around 1.95583, when it became part of the European Exchange Rate Mechanism II in 2020). Bulgaria adopted the Euro and left behind its own currency after Croatia, at the beginning of 2025, moved from the kuna to the Euro. Among the contrasts in the two countries are their experiences in the lead-up to both of them entering ERMII on July 10, 2020. Bulgaria had a currency board which it maintained after entering ERMII, and it frequently intervened to maintain the 1.95583 rate - the deviation of the market value of the leva around 1.95583 was normally in hundredths of percent, as it had been in the period prior to Bulgaria joining ERMII. Croatia did not have a currency board, but rather what has usually been termed a managed floating rate, with periodic interventions by the central bank to stabilize fluctuations, and It set its entry rate to ERMII at the market exchange rate at the time of entry, committing its central bank to intervene periodically to maintain the 7.53450 fix within the ERMII band (+/-15%) which is generally applicable within ERMII. After the moves by Bulgaria and Croatia, Denmark is now the sole member of ERMII, with a ±2.25% band around 7.46038 kroner per euro.

After 25 years of negotiation, and overcoming strenuous opposition by major economic groups, such as many European Union farmers, the Mercosur southern common market group of South America (Argentina, Brazil, Paraguay, and Uruguay) has just signed (January 17) a freer trade agreement (the EU-Mercosur Partnership Agreement, EMPA for short), at the annual Mercosur summit, covering nearly every economic sector of both groups, adding up to (according to many estimates) 90% of EU-Mercosur trade. A ratification vote (with timing uncertain) by the European Parliament is a next step, along with ratification by each of 31 European signatories - ratification votes by each of the four Mercosur countries are regarded as certain, given the prospect of increased security for access to the European Union by Mercosur country agricultural sectors. By several measures, the agreement will cover roughly 20 per cent of the world economy, and, the approach to freer trade at this moment is widely noted as a strong contrast to the United States moves toward restrictions and barriers to trade with other countries, with US trade measures in 2025 providing impetus to the EU-Mercosur deal, which would be the largest in history, and also the most comprehensive, covering topics such as intellectual property, trade in services, government procurement and state-owned firms. Among the implications of the EU-Mercosur deal is that there is talk of how world coverage of the agreement could expand, as some other South America countries are applying to join the group, and there is also talk of movement towards a Mercosur deal with the BRICS group (of which Brazil is a major overlap with the EU-Mercosur trade deal), and also with a number of Asian countries (China and India are both members of BRICS, and India is the 2026 chair of BRICS).

(World Currency Observer will next be updated on February 2, 2026. Visit Search to look at past issues of World Currency Observer (brochure edition). For permission-to-quote enquiries, e-mail World Currency Observer at WCO@briargreen.com.)